Yes, you may be able to buy a house while carrying student loan debt. Student loans do not automatically disqualify you from getting a mortgage. However, your monthly student loan obligation can affect your debt-to-income ratio, borrowing power, mortgage options, and the amount of home you may qualify to purchase.

With nearly $1.84 trillion in outstanding student loan debt spread across more than 42 million Americans, it is no surprise that student loans are one of the biggest concerns we hear from prospective homebuyers.

Here is the good news: student loans do not disqualify you from getting a mortgage. But they do affect your debt-to-income ratio, and the way lenders calculate that impact varies depending on the loan program. Understanding these differences can be the key to getting approved.

Key Takeaways

- Student loan debt does not automatically prevent you from buying a home.

- Lenders focus heavily on your monthly student loan payment and overall debt-to-income ratio.

- FHA, Fannie Mae, Freddie Mac, and VA loans may calculate student loan obligations differently.

- A documented income-driven repayment payment may improve qualification under certain loan programs.

- Comparing mortgage programs before applying can help you find the most suitable option for your financial situation.

Not sure how your student loans affect your mortgage options? A mortgage professional can review your documented payment, debt-to-income ratio, income, credit, and available loan programs before you begin home shopping. Contact My Easy Mortgage to discuss your situation.

Do Student Loans Affect Buying a House?

Student loans affect buying a house because they are generally included in the lender’s evaluation of your monthly financial obligations. The lender does not look only at the total amount you owe. Your documented monthly payment, repayment status, credit history, income, assets, and selected mortgage program can all influence the underwriting decision.

Student loan debt can affect your mortgage application in several ways.

Student Loans Can Increase Your Debt-to-Income Ratio

Your debt-to-income ratio compares your recurring monthly debt payments with your gross monthly income. A higher student loan payment can increase your DTI and potentially reduce the mortgage amount for which you qualify.

Payment History Can Affect Your Credit Profile

Consistently making student loan payments on time can support a stronger credit history. Missed payments, delinquency, collections, or default may negatively affect your credit profile and make mortgage qualification more difficult.

Student Loans Can Affect Your Borrowing Power

Even when you have a strong income and credit score, a high monthly student loan obligation may leave less room for a future housing payment. This can affect your maximum eligible mortgage payment and homebuying budget.

The important point is that mortgage and student loan debt must be evaluated together. Two borrowers with the same student loan balance may receive different qualification results because their monthly payments, incomes, credit profiles, and selected mortgage programs are different.

How Lenders Factor Student Loans Into Your DTI

Your debt-to-income ratio is your total monthly debt payments divided by your gross monthly income. It is one of the most important numbers in your mortgage application.

Student loans count toward that monthly debt figure, even if your loans are deferred, in forbearance, or on an income-driven repayment plan with a $0 payment. The qualifying amount depends on the mortgage program and the documentation available to the lender.

The basic DTI formula is:

Total monthly debt payments ÷ gross monthly income × 100

For example, consider a borrower with:

- $6,000 in gross monthly income

- $300 in student loan payments

- $400 in car payments

- $100 in minimum credit card payments

- $1,800 in estimated monthly housing expenses

The total monthly debt would be $2,600.

$2,600 ÷ $6,000 × 100 = 43.3% DTI

The lender would then evaluate whether that DTI is acceptable based on the selected mortgage program, credit profile, reserves, automated underwriting findings, and other qualification factors.

When your credit report shows a $0 monthly payment, lenders do not always use zero. Instead, they may calculate a qualifying payment based on your outstanding balance, repayment status, documentation, and mortgage program.

This is why someone asking, “How can I buy a house with student loan debt?” should begin by confirming which payment a mortgage lender will use before estimating affordability.

FHA, Conventional, and VA Loans Use Different Rules

FHA, conventional, and VA loans do not always calculate student loan debt in the same way. The differences can have a meaningful effect on your DTI and mortgage eligibility.

| Mortgage program | General treatment of student loan debt |

|---|---|

| FHA | May use the reported payment or a calculated payment based on the balance when the reported payment is zero |

| Fannie Mae | May allow a documented $0 income-driven repayment payment |

| Freddie Mac | Generally uses 0.5% of the balance when a $0 payment is reported, subject to current documentation and recertification rules |

| VA | Uses its own qualifying calculation and may exclude certain deferred loans when specific requirements are met |

Mortgage guidelines can change, and lenders may apply additional underwriting requirements. Your loan officer should confirm the current rule that applies to your file.

FHA Loans and Student Loan Debt

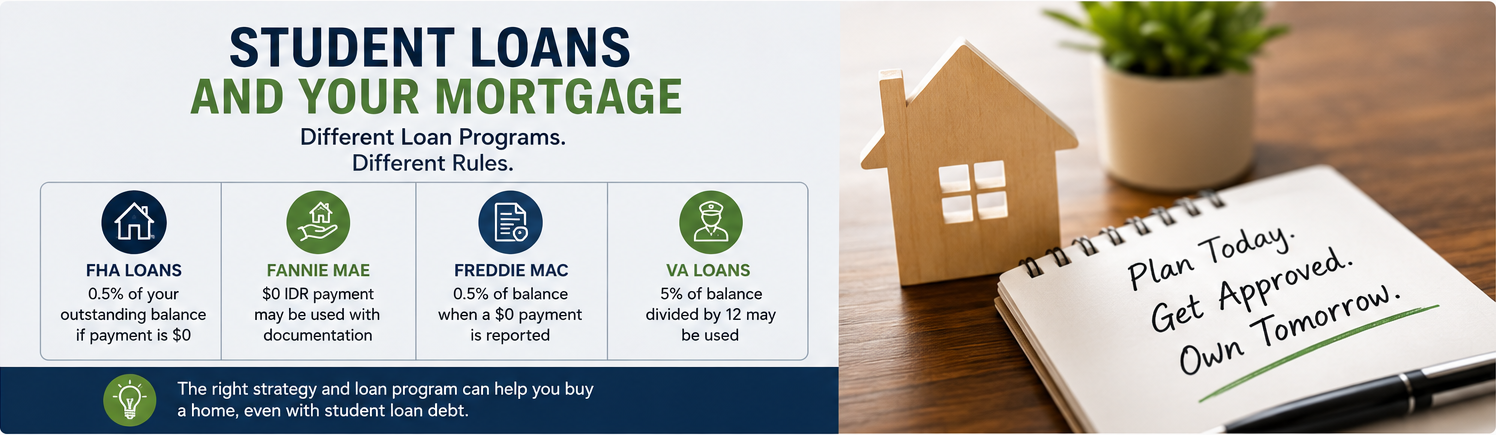

FHA loans use 0.5% of your outstanding student loan balance as your monthly payment whenever your credit report shows $0.

If you owe $60,000 in student loans, FHA underwriting may add $300 per month to your DTI, regardless of whether you are currently making payments.

$60,000 × 0.5% = $300 per month

If your income-driven repayment plan has an active documented payment above $0, the lender may be able to use that actual amount instead, subject to the applicable FHA requirements and lender documentation.

FHA financing may still be a useful option for borrowers with student loan debt, especially when the borrower has an acceptable credit profile, sufficient income, and manageable overall monthly obligations.

Fannie Mae Conventional Loans

Conventional loans through Fannie Mae can offer favorable treatment for certain borrowers using income-driven repayment plans.

If you are on an income-driven repayment plan and your documented payment is $0, Fannie Mae allows lenders to use that documented $0 payment for qualifying purposes.

That can create a more favorable DTI and potentially improve your chance of qualifying for your desired home price.

However, the lender must obtain acceptable student loan documentation verifying that the actual monthly payment is $0. A credit report showing $0 by itself may not be sufficient.

For deferred loans or loans in forbearance, the lender may need to use either:

- 1% of the outstanding student loan balance

- A fully amortizing payment based on the documented repayment terms

The exact calculation depends on the documentation and current underwriting guidelines.

Freddie Mac Conventional Loans

Freddie Mac takes a different approach.

When a $0 payment is reported, Freddie Mac generally requires the lender to use 0.5% of the outstanding student loan balance unless acceptable documentation supports another payment greater than zero.

For a $60,000 student loan balance:

$60,000 × 0.5% = $300 per month

Additional requirements may apply when the borrower must recertify income before or near the first mortgage payment date or when the documented payment is expected to increase.

This is an important distinction for borrowers comparing conventional mortgage options. A loan eligible through Fannie Mae may produce a different DTI result from one evaluated under Freddie Mac guidelines.

VA Loans and Student Loan Debt

VA loans have their own student loan calculation.

A commonly used VA calculation is 5% of the outstanding student loan balance divided by 12 months.

For a $60,000 balance:

$60,000 × 5% ÷ 12 = $250 per month

VA loans also have a unique potential advantage. If student loans are deferred for at least 12 months beyond the anticipated closing date, the obligation may be excluded from the DTI calculation when the required documentation and VA conditions are satisfied.

However, VA qualification is not based on DTI alone. The lender may also evaluate residual income, credit, employment, assets, occupancy, and other VA underwriting requirements.

Can You Qualify With a $0 Income-Driven Repayment Payment?

A documented $0 income-driven repayment payment may be used under certain mortgage programs, but the treatment is not the same for every loan type.

Fannie Mae may allow a lender to qualify a borrower using a documented $0 IDR payment. FHA and Freddie Mac may require a calculated payment when the credit report shows zero, depending on the available documentation and current guidelines.

This is why borrowers should obtain current student loan statements and repayment-plan documentation before beginning mortgage preapproval.

Do not assume that a payment displayed as $0 on your credit report will automatically be treated as $0 during underwriting.

A mortgage lender may request:

- A recent student loan statement

- Documentation of your repayment plan

- Confirmation of your required monthly payment

- The outstanding balance

- Evidence of deferment or forbearance

- Information about an upcoming income recertification

- Fully amortizing repayment terms

The right mortgage program can change the calculation. My Easy Mortgage can compare conventional, FHA, VA, and other available mortgage options based on your documented student loan payment and complete financial profile.

The SAVE Plan Is Gone: What Now?

On March 10, 2026, the Saving on a Valuable Education, or SAVE, plan was canceled by the Eighth Circuit Court of Appeals, leaving millions of borrowers considering what to do next.

Borrowers affected by student loan repayment changes should review their current status directly through their loan servicer and Federal Student Aid repayment resources.

The original recommendation for borrowers was to switch to income-driven repayment before applying for a mortgage. However, available income-driven repayment plans, payment calculations, recertification requirements, and borrower eligibility can change.

An eligible income-driven repayment plan may lower the documented monthly payment used during mortgage qualification. Some qualifying borrowers may have a payment as low as $0, while others will have a payment based on income, family size, loan type, and applicable repayment rules.

Borrowers on an income-driven repayment plan generally need to recertify their income and family size periodically. Remaining balances may also qualify for forgiveness after the required repayment period, depending on the plan and the borrower’s eligibility.

Before changing repayment plans solely to improve mortgage qualification, consider speaking with both your student loan servicer and a qualified mortgage professional. A lower monthly payment may improve DTI, but the decision should also account for interest, repayment duration, potential forgiveness, tax considerations, and long-term financial goals.

What If Your Student Loans Are Deferred or in Forbearance?

Deferred or forbearance status does not necessarily mean a lender can ignore your student loan debt.

Even when no payment is currently due, many mortgage programs require the lender to calculate a qualifying monthly obligation. The lender may use a percentage of the outstanding balance or a fully amortizing payment based on the loan terms.

The calculation can vary among FHA, Fannie Mae, Freddie Mac, and VA loans.

Before applying, collect documentation showing:

- Your current student loan status

- The outstanding balance

- The scheduled repayment date

- The expected monthly payment

- The length of the deferment or forbearance

- Any repayment-plan terms

Providing complete documentation early can reduce underwriting delays and help your mortgage professional identify the most appropriate program.

Can You Buy a House With Student Loans in Default?

Buying a home with student loans in default can be more difficult, but the result depends on the type of student loan, credit history, selected mortgage program, and current status of the debt.

Default may affect:

- Your credit score

- Your payment history

- Government-backed mortgage eligibility

- Federal debt checks

- Collections or judgments

- Your overall risk profile

- The mortgage programs available to you

Borrowers with defaulted federal student loans may need to resolve or rehabilitate the debt before becoming eligible for certain government-backed mortgage programs.

Do not wait until you have found a property to address defaulted student loans. Speak with your student loan servicer and a mortgage professional before beginning the home search so you can understand the steps required for qualification.

Strategies for Buying a Home With Student Loans

Student loans are only one part of your mortgage profile. The following strategies may help improve your qualification position.

Get on an Eligible IDR Plan and Document the Payment

An income-driven repayment plan may produce a lower required monthly payment than a standard repayment plan. However, eligibility and mortgage treatment vary.

Obtain documentation showing the current required payment before applying.

Choose the Right Loan Program for You

FHA, Fannie Mae, Freddie Mac, and VA loans can calculate student loan debt differently. Comparing programs may identify a structure that better fits your income, credit, student loan payment, down payment, and homebuying goals.

Pay Down High-Interest Debt First

Paying down a smaller credit card or personal loan with a high monthly payment may improve your DTI more effectively than making an equivalent lump-sum payment toward a large student loan balance.

Before moving significant funds, ask your mortgage professional to compare how different debt-paydown strategies would affect your qualification.

Review Your Credit Reports

Check your credit reports for incorrect balances, duplicate student loan accounts, outdated payment amounts, or inaccurate delinquency information.

Disputing legitimate errors before applying can help prevent unnecessary underwriting complications.

Avoid Taking on New Debt

New credit cards, auto loans, personal loans, and large financed purchases can increase your DTI and lower your mortgage qualification amount.

Avoid applying for new debt before preapproval and throughout the mortgage process unless you have discussed it with your loan officer.

Build Savings and Financial Reserves

In addition to the down payment and closing costs, available reserves may strengthen your overall mortgage profile. Reserves can also provide financial protection against unexpected home repairs, moving costs, and other expenses.

Get Preapproved Before Shopping

Mortgage preapproval helps determine:

- Which student loan payment the lender will use

- Which mortgage programs may be available

- Your estimated borrowing range

- Your expected monthly housing payment

- The documents required for underwriting

- Potential issues that should be resolved before making an offer

Work With a Lender Who Understands Student Loan Guidelines

Work with a lender who understands these guidelines. My Easy Mortgage has experience with student loan programs and can help answer pressing questions for homebuyers who have student loan debt.

A knowledgeable mortgage broker can compare available lenders and programs rather than assuming one calculation applies to every borrower.

Documents to Prepare Before Applying

Preparing your documents early can make the preapproval and underwriting process more efficient.

You may need:

- Recent student loan statements

- Repayment-plan confirmation

- Documentation of the required monthly payment

- Deferment or forbearance documentation

- Recent pay stubs

- W-2 forms

- Tax returns, when required

- Bank and investment statements

- Identification

- Employment information

- Documentation for additional income

- Statements for other debts

- Information about funds for the down payment and closing costs

The lender may request additional documentation based on your mortgage program, employment type, income structure, credit history, and student loan status.

Buying a Home With Student Loans in Tampa Bay

For borrowers searching for a mortgage broker in Tampa, FL, student loan debt should be reviewed as part of the complete homebuying strategy.

Home prices, property taxes, homeowners insurance, flood zones, homeowners association fees, and available down payment funds can all affect affordability in Tampa Bay. Your student loan payment must be considered together with these local housing expenses.

Whether you are buying in Wesley Chapel, Land O’ Lakes, Tampa, or another Florida community, getting preapproved before viewing homes can help establish a realistic budget.

A Tampa mortgage broker can compare available programs and explain how your student loan payment may be treated by different lenders.

My Easy Mortgage works with first-time homebuyers, repeat buyers, homeowners considering refinancing, and borrowers with different income and debt profiles.

Frequently Asked Questions

Can I Buy a House if I Have Student Loan Debt?

Yes. Student loans do not automatically prevent mortgage approval. Lenders evaluate your monthly student loan payment, income, credit profile, assets, other debts, and proposed mortgage payment.

Do Student Loans Affect How Much Mortgage I Can Qualify For?

Yes. A higher qualifying student loan payment increases your debt-to-income ratio and may reduce the mortgage amount you can afford or qualify to borrow.

How Do Lenders Calculate Student Loans With a $0 Payment?

The calculation depends on the mortgage program, repayment status, credit report, documentation, and underwriting guidelines. Some programs may use a documented $0 payment, while others may calculate a percentage of the outstanding balance.

Can I Get an FHA Loan With Student Loan Debt?

Potentially, yes. FHA lenders include a qualifying student loan payment when calculating DTI, but having student loan debt alone does not disqualify you from receiving an FHA mortgage.

Can Deferred Student Loans Be Excluded From My DTI?

Not always. Many mortgage programs still require a qualifying payment for deferred student loans. Certain VA circumstances may permit exclusion when the deferment extends at least 12 months beyond closing and all applicable documentation requirements are met.

Should I Pay Off Student Loans Before Buying a House?

Not necessarily. Paying down a smaller debt with a high monthly payment may improve your DTI more effectively than making a large payment toward a student loan balance. Ask a mortgage professional to compare the qualification impact before using your available savings.

Should I Get Preapproved if I Have Student Loans?

Yes. Preapproval can identify the student loan payment the lender will use, the mortgage programs available to you, and the approximate home price that fits your complete financial profile.

Student Loans Do Not Have to End Your Home Search

Student loans are a factor in your mortgage approval, but they are not a death sentence.

The borrowers who struggle are usually the ones who do not know the rules going in. The borrowers who get approved are often the ones who plan ahead and work with a lender who knows how to structure the deal around their real financial picture.

Whether you are a first-time buyer or looking to refinance, My Easy Mortgage is a reputable mortgage broker with offices at:

Wesley Chapel Office

2405 Creel Lane, Suite 102

Wesley Chapel, FL 33544

Land O’ Lakes Office

16703 Early Riser Avenue, Suite 266

Land O’ Lakes, FL 34638

The My Easy Mortgage team can help you understand how student loans may affect your DTI, borrowing power, and mortgage options.

Call (813) 513-9846 or contact My Easy Mortgage to discuss your mortgage needs and begin your personalized mortgage review.

Mortgage guidelines, student loan repayment programs, and qualification requirements can change. Loan approval depends on the borrower’s complete financial profile, selected program, lender requirements, property, and underwriting review.